Green Transition

Integrity Sorting Changes the Voluntary Carbon Market Picture

Not all carbon credits are one quality bucket. ICVCM integrity standards, ICAO CORSIA eligibility, and Microsoft's January 2026 removal procurement, read separately for the 2026 outlook.

Thesis

(Source: ICVCM, The Core Carbon Principles)

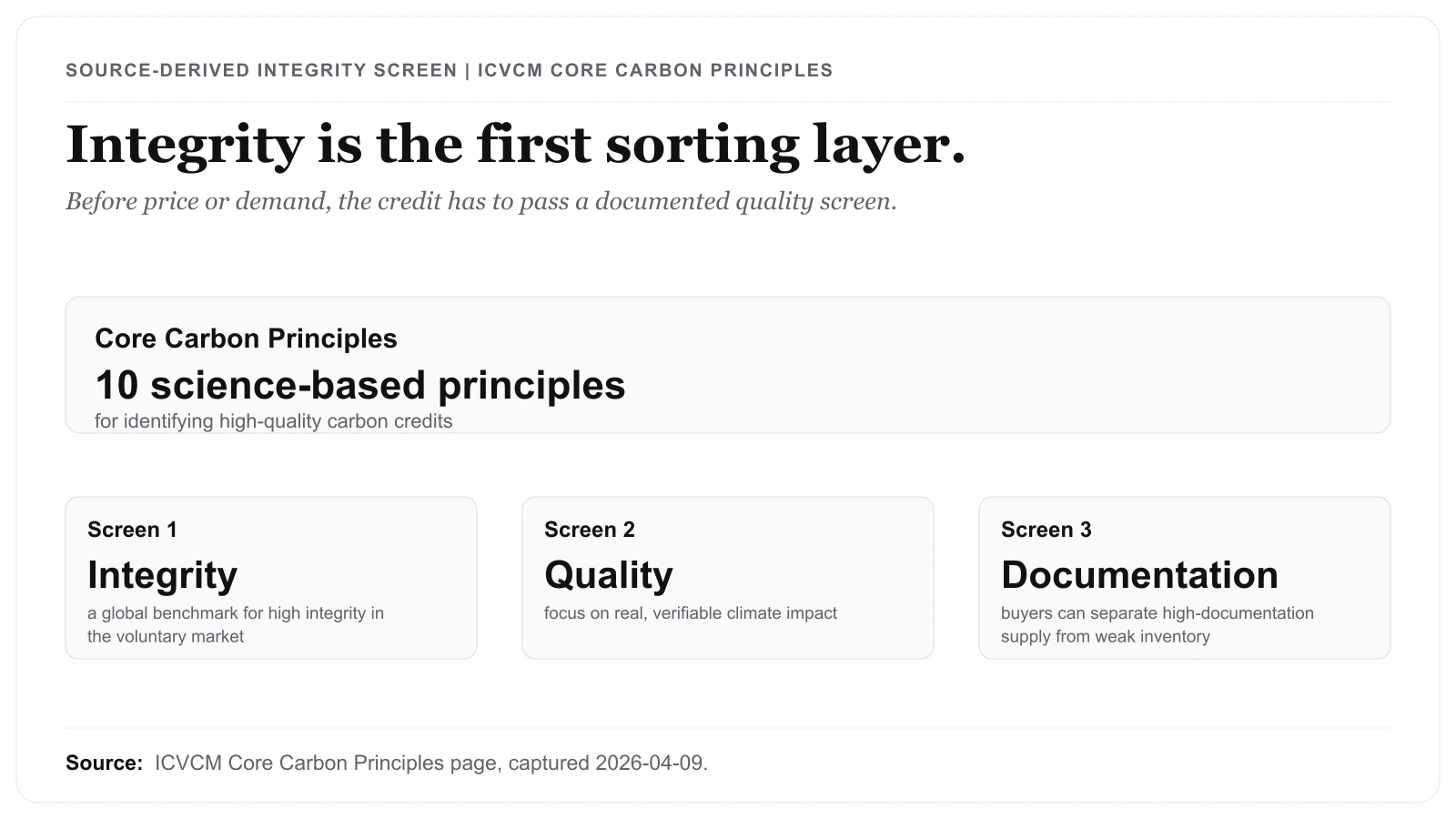

The ICVCM Core Carbon Principles page settles one prerequisite before any credit comparison can begin: it puts the definition of "high integrity" in writing. That written definition is where our reading started. From there the trail ran forward — into ICAO's CORSIA phase tables (2024-2026 and 2027-2029), then into Microsoft's January 2026 procurement detail (60+ projects, 78+ million metric tonnes). Saying credits differ in quality is only fair once that definition is pinned down; with it fixed, the rest of the comparison held up.

Say "voluntary carbon market" out loud and it still lands like one undifferentiated pool. The official sources suggest something narrower and more useful. In 2026, the market is being filtered through three different screens:

- integrity benchmarks,

- programme eligibility rules, and

- the procurement behavior of documented repeat buyers.

That does not mean the market is suddenly simple. It does mean broad claims about "the voluntary carbon price" or "all offsets" are less useful than they used to be.

Source Evidence Snapshot

The hero card already carries Microsoft's CDR procurement figures. The body evidence keeps the two rule-setting layers visible: ICVCM integrity and ICAO CORSIA eligibility. Microsoft's demand detail remains a source note, so the page does not repeat the same buyer PDF surface twice.

Source-derived integrity screen based on the ICVCM Core Carbon Principles page, captured 2026-04-09: ten science-based principles for identifying high-quality carbon credits and a global benchmark for high integrity in the voluntary carbon market. The wording is source-derived; the layout is ours.

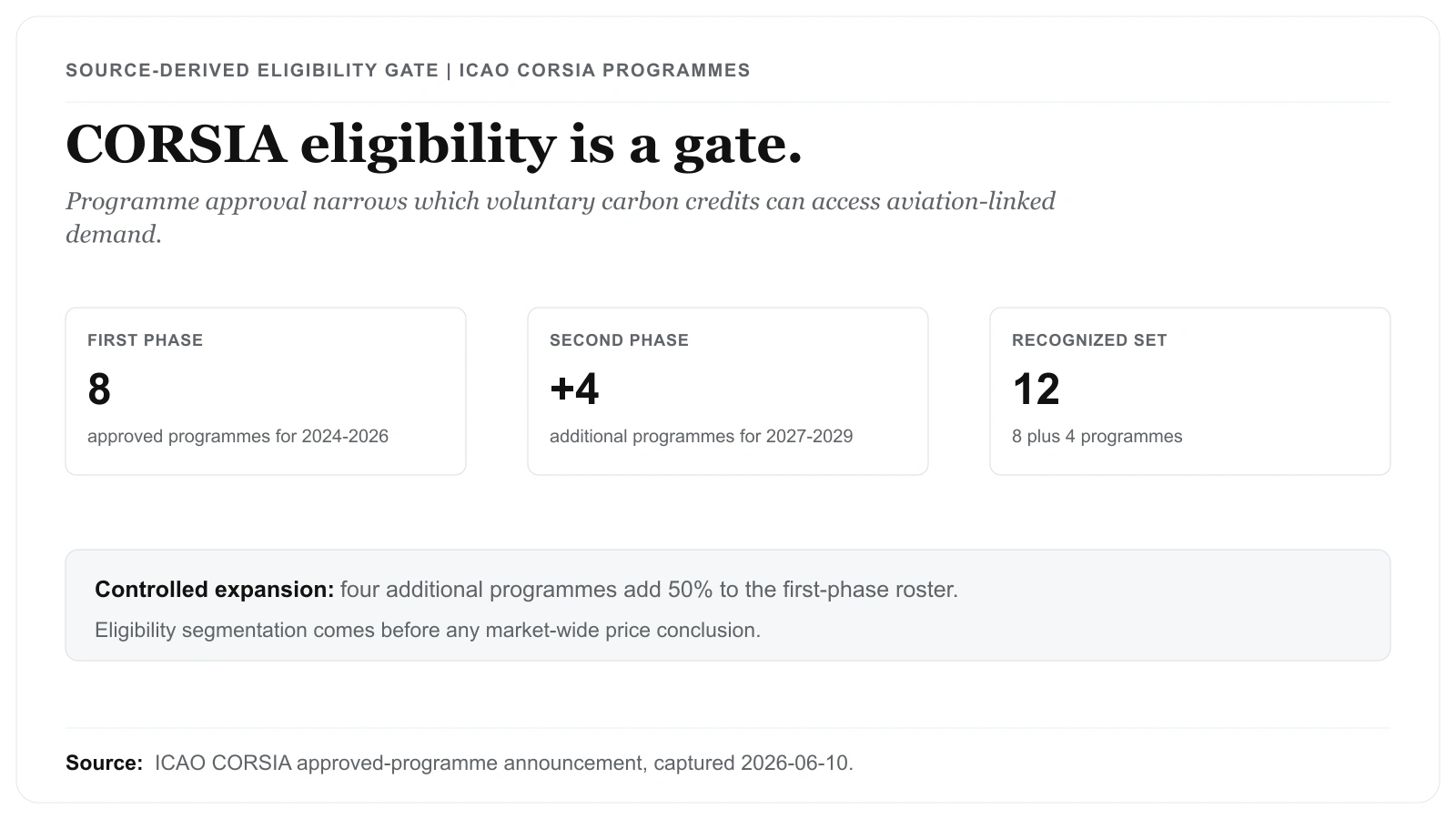

Source-derived eligibility gate based on ICAO's expanded CORSIA approved programmes, captured 2026-06-10: eight programmes for the 2024-2026 first phase and four additional for the 2027-2029 second phase. The 12 recognized-programme set and 50% expansion are article math from those figures.

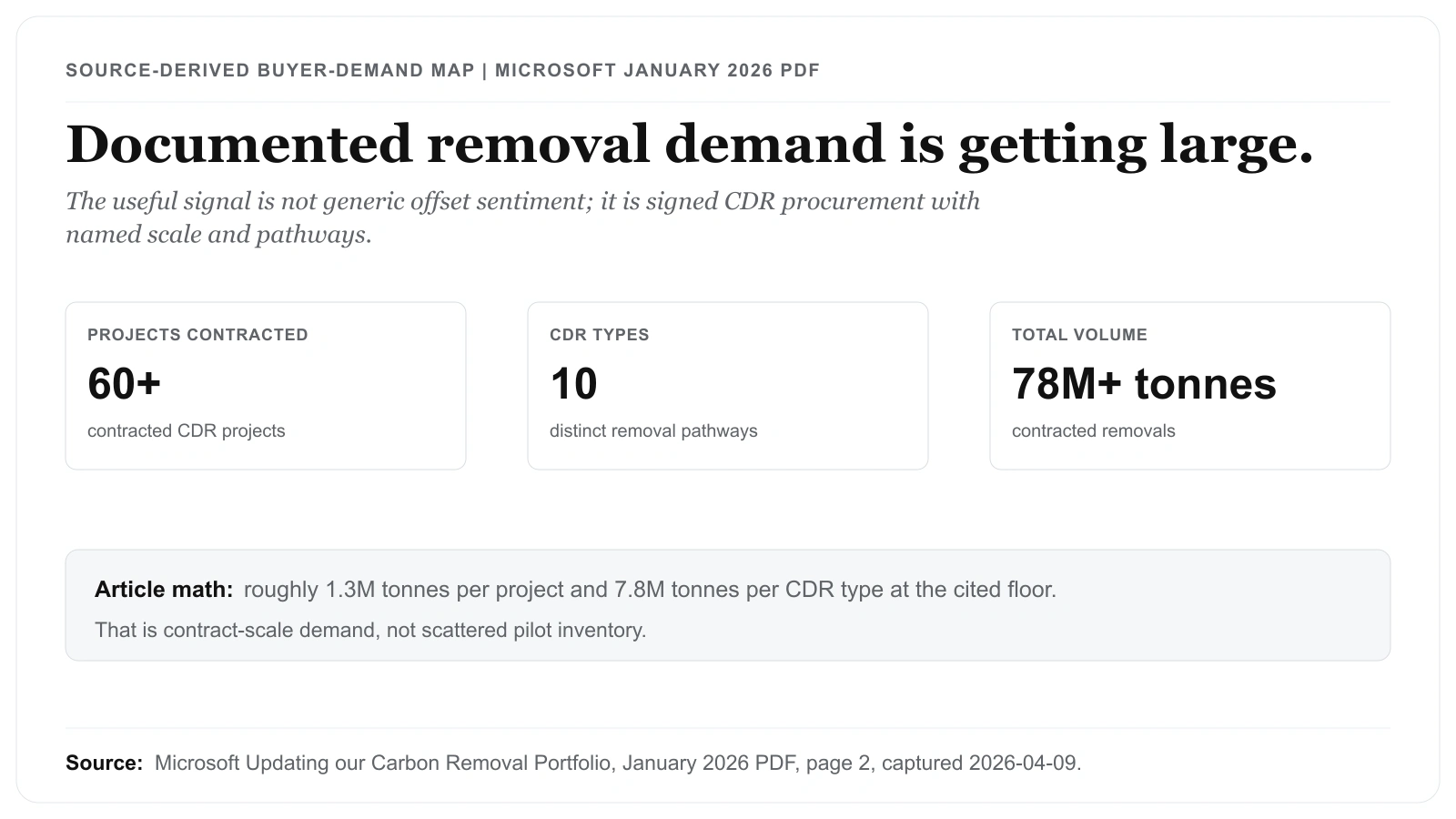

Source note: Microsoft, Updating our Carbon Removal Portfolio (January 2026 PDF), captured 2026-04-09 from page 2. The buyer-demand evidence remains the same: more than 60 projects, 10 distinct types of CDR, and more than 78 million metric tonnes.

What These Sources Support

1. Integrity is no longer a side note

The ICVCM page does not present the Core Carbon Principles as a minor label. It calls them a science-based framework for identifying high-quality credits and a global benchmark for high integrity in the voluntary market. That matters because it formalizes a quality screen that many buyers used to apply informally, if at all.

2. Eligibility is becoming more program-specific

The ICAO page shows that access to CORSIA demand is not open-ended. Eight programmes are approved for the 2024-2026 first phase and four additional programmes for the 2027-2029 second phase, so the recognized set widens to twelve programmes total (8 + 4) — a 50% expansion (4 ÷ 8) layered on top of the first-phase roster rather than a fresh slate. That is a controlled widening of access, not an open gate. Even without assigning prices, the gated count alone tells you the market is not one undifferentiated bucket of interchangeable credits.

3. Documented demand is concentrating in removal procurement

Microsoft's January 2026 portfolio update gives a useful demand signal because it is specific rather than promotional. The company says it contracted more than 60 projects across 10 distinct CDR pathways, totaling more than 78 million metric tonnes. Sizing that against itself sharpens the read: 78 million tonnes spread over 60-plus projects implies an average of roughly 1.3 million tonnes contracted per project (78 ÷ 60), and across 10 distinct CDR types that is on the order of 7.8 million tonnes of demand per pathway (78 ÷ 10). Those are contract sizes, not pilot tickets. This is not scattered experimentation — it is large corporate demand concentrating in screened removal supply rather than generic offset inventory, at a per-project scale most voluntary inventory never sees.

What These Sources Do Not Prove

- They do not prove that every voluntary credit deserves a premium.

- They do not prove one clearing price for the whole market.

- They do not prove that every corporate net-zero claim is high integrity.

Those limits are important. The sources above support market segmentation, not a blanket endorsement of the category.

A More Useful Way to Read the Market in 2026

If you strip away the marketing language, the official evidence points toward a simpler operating view.

First, check whether a programme or methodology clears a recognized integrity benchmark. Second, check whether a compliance-adjacent buyer set like CORSIA recognizes the programme. Third, check whether repeat corporate buyers are actually signing size with that type of supply.

That sequence is more useful than starting with a headline about the whole market. It also reduces the risk of treating low-documentation inventory and high-documentation removals as if they belong in the same quality bucket.

What to Monitor From Here

For this topic, a good refresh loop is straightforward:

- Recheck ICVCM pages for updates to CCP-related standards and approved methodologies.

- Recheck ICAO CORSIA eligibility pages when programme approvals or phase rules change.

- Recheck major buyer disclosures such as Microsoft procurement updates to see whether demand concentration is broadening or narrowing.

That workflow keeps the article grounded in rule text, approved-programme lists, and signed procurement rather than in vague sentiment.

A practical 2026 nuance is timing risk between these three layers. Integrity language can update on one timeline, programme eligibility can update on another, and buyer contracting can shift quarter by quarter. If one layer moves while the other two lag, price and quality signals can diverge for months. That is why this market is better read as an evidence stack that is refreshed in sequence, not as a single headline indicator.

Quick Documentation Threshold Before You Trust Supply

If a credit programme or supplier cannot show all three layers in documentation, treat it as lower-confidence inventory. Layer one is integrity language aligned with the ICVCM benchmark framework. Layer two is programme-level eligibility context in ICAO CORSIA phase tables (2024-2026 and 2027-2029). Layer three is contract-scale buyer disclosure like Microsoft's January 2026 update (60+ projects, 10 CDR types, 78+ million metric tonnes). This is a screening rule, not a price forecast.

What Changes the Market Read

The official sources do not support the idea of one uniform voluntary carbon market. They support a more segmented reading:

- integrity screens matter more,

- programme eligibility matters more, and

- documented buyer evidence matters more.

In 2026, the strongest signals come from exactly those three layers. That is where the market is being sorted.

Related reads: