Energy & Commodities

The EIA Release Calendar Puts Crude Risk and Energy Stocks on a Clock

No fixed oil-price call here. The EIA STEO schedule anchors a 2026 read on energy-stock and inflation sensitivity, with IEA timing kept as a source note.

Thesis

(Source: U.S. EIA STEO Release Schedule)

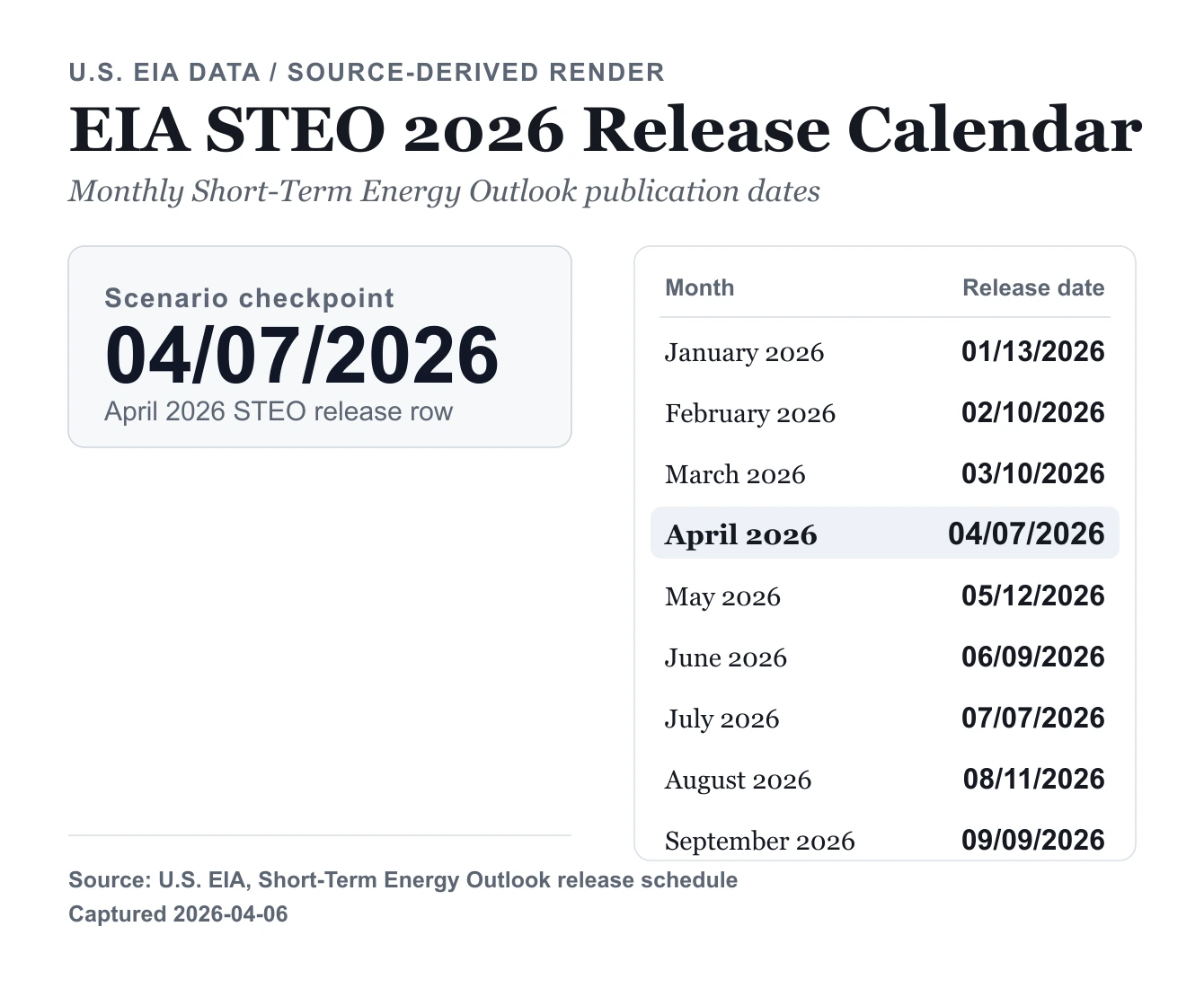

The popular "$90 oil is coming" framing went into this note as the claim to support; it came out as the claim that would not stand up. Checked against the primary sources we pulled — the EIA STEO schedule, the IEA OMR product page (next release 14th April 2026), the WPSR timing page — each one returns a dated release window, and none returns a committed price level. So no forced number. What got logged instead: each scheduled drop, plus the 2026-04-07 STEO row, as the checkpoints that would actually confirm or weaken a price-stress read.

When oil headlines move faster than the underlying data calendar, the more reliable approach is to map a price-stress scenario to scheduled primary-source releases, then update the read as each release lands. For market-risk work, the more reliable approach is to map a price-stress scenario to scheduled primary-source releases, then update the read as each release lands.

The 2026 thesis is that crude-price stress should be handled as a monitored scenario, not as a static forecast. Upstream, integrated majors, services, and inflation-sensitive assets react through different channels, so the release calendar matters as much as the price label.

That discipline also limits overfitting. A single price print can reflect positioning, weather, freight, inventories, policy headlines, or geopolitical risk premia. A publishable scenario needs to identify which official release would confirm the pressure and which release would weaken it.

Source Evidence Snapshot

The hero image already carries the EIA STEO release schedule table, including the April 7, 2026 row. The body evidence avoids repeating that same source surface.

The IEA OMR timing is kept as a linked source note instead of a thin metadata crop: Source note: IEA Oil Market Report data product page, captured 2026-04-06, metadata block with next release date (14th April 2026).

Evidence visual of the EIA WPSR release windows — figures from the EIA Weekly Petroleum Status Report schedule, captured 2026-04-06 (

Evidence visual of the EIA WPSR release windows — figures from the EIA Weekly Petroleum Status Report schedule, captured 2026-04-06 (after 10:30 a.m. and after 1:00 p.m. ET on Wednesday). The numbers are the source's; the layout is ours.

This evidence set is intentionally calendar-focused. The hero image keeps the April 2026 STEO table row visible, while the retained body panel focuses on the weekly petroleum-data timing that can reprice the scenario between monthly releases.

Event Calendar That Can Reprice the Oil Narrative

For near-term market interpretation, these timestamps matter more than social-media momentum:

2026-04-07: EIA STEO release window.2026-04-08: EIA AEO next release date.2026-04-14: IEA OMR next scheduled release (10:00 Paris time).- Weekly cadence: EIA WPSR summary files typically publish after

10:30 a.m.ET on Wednesdays, with additional files after1:00 p.m.ET.

Reading the gaps between those dates is itself a signal. The three monthly checkpoints are front-loaded: STEO (2026-04-07) to AEO (2026-04-08) is one day, then AEO to OMR (2026-04-14) is six days, so the entire monthly confirm-or-weaken sequence spans exactly seven days — 2026-04-07 to 2026-04-14, one full week. Two of the three primary releases land inside the first 48 hours, meaning most of the new information that can reprice the scenario arrives at the front of the week and is then tested by data, not refreshed by it, for the six days until the OMR. Inside a single WPSR Wednesday, the two posting windows (10:30 a.m. and 1:00 p.m. ET) sit 2.5 hours apart, so the weekly inventory read is fully on the tape within a 2.5-hour band rather than drip-fed through the session.

What a Crude-Price Stress Scenario Usually Means Across Energy Equity Buckets

Upstream Producers

Key variables to monitor:

- production discipline versus growth spending,

- hedging profile,

- lifting-cost structure,

- capital-return policy quality under different oil bands.

Integrated Majors

Integrated majors often provide a smoother risk profile. Upstream strength can be partially offset or stabilized by downstream and trading segments, depending on margin conditions.

For diversified market exposure, these names can function as lower-volatility oil-beta relative to pure upstream exposure.

Oilfield Services

Oilfield services are typically second-order beneficiaries. The sector response depends less on spot oil itself and more on whether producers convert higher prices into higher capex and activity.

The practical trigger is not the first day of a price spike. It is whether sustained price strength survives multiple reporting cycles.

Inflation Transmission: Why the Oil Move Can Outrun the Energy Trade

Higher crude can lift more than energy equities. It can also pressure broad inflation-sensitive exposures through fuel, freight, and input-cost channels.

That creates a market-risk tension:

- one sleeve may benefit directly from oil strength,

- another sleeve may suffer from higher input costs, tighter financial conditions, or renewed inflation sensitivity.

This is why a crude scenario should be linked to a cross-asset risk plan, not traded in isolation.

A Practical Scenario Grid for 2026

Use this as an operating template and update after each official release.

Scenario A: Sustained Tightness

If STEO and OMR updates continue to reinforce tighter balances and no major demand deterioration appears, the market can support a durable higher-price regime.

Typical equity read-through:

- strongest relative performance in upstream,

- constructive setup for selected services if activity follows,

- inflation-sensitive duration assets may remain fragile.

Scenario B: Range-Bound Repricing

If releases are mixed, oil can remain volatile inside a wide range around the narrative level rather than trend in one direction.

Typical equity read-through:

- stock selection and balance-sheet quality matter more than headline oil beta,

- integrated exposure can reduce drawdown volatility,

- tactical rather than aggressive directional sizing often works better.

Scenario C: Demand-Led Reset

If demand revisions weaken while supply risk premium compresses, a sharp pullback scenario can emerge.

Typical equity read-through:

- high-beta upstream can derate fastest,

- services can lag on delayed capex response,

- inflation pressure can ease, changing cross-asset leadership.

Scenario Risk Checklist

- define the release dates that would invalidate the thesis,

- separate directional oil exposure from quality-factor equity exposure,

- avoid concentration that assumes one geopolitical path,

- plan scenario updates around release timestamps, not only price headlines,

- keep explicit downside markers for scenario failure.

Related reads:

- Strait of Hormuz in 2026: Flow Exposure and Risk-Asset Transmission

- Investing in Carbon Credits Guide

Data-Update Workflow for This Scenario

A practical way to keep this framework current is to run a fixed release-day routine:

- Update the latest STEO release assumptions and compare monthly deltas in supply-demand language.

- Cross-check whether AEO structural assumptions reinforce or challenge monthly directional signals.

- Read OMR release notes for global balance shifts and timing risks.

- Use WPSR publication windows to track near-term inventory and refinery-throughput changes in a consistent weekly cadence.

The objective is consistency. A repeatable workflow reduces the chance of overreacting to one headline and improves exposure discipline under fast-moving oil narratives.