Market & Macro

Verify Your Broker Before You Pick a Single U.S. Stock

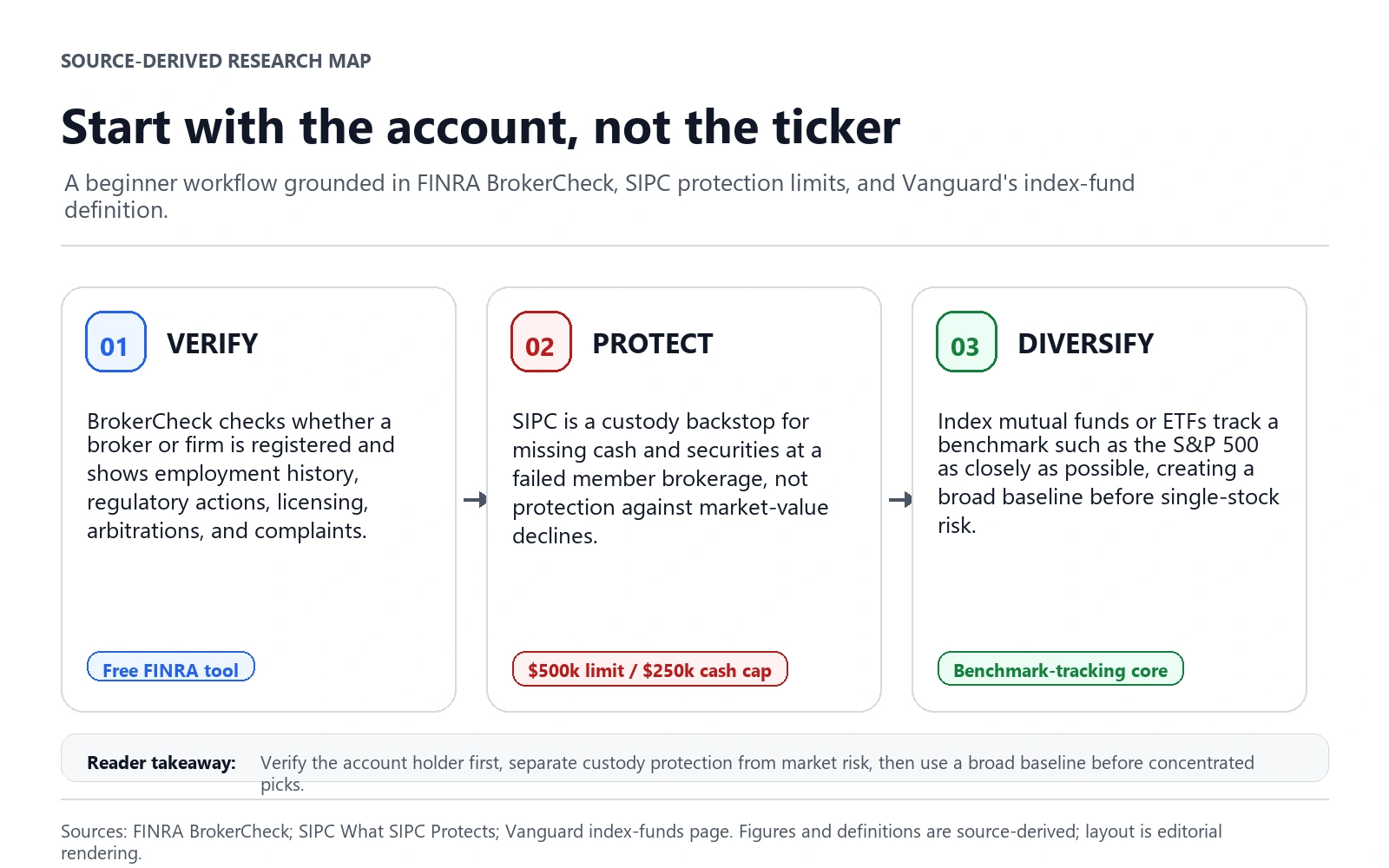

Before a single individual stock: verify the broker, understand SIPC limits, and set a broad index-fund baseline. A 2026 investor-safety starting point.

Thesis

(Sources: FINRA BrokerCheck, SIPC - What SIPC Protects, Vanguard - Index funds)

$500,000, including up to $250,000 for cash, is the protection ceiling SIPC prints on its "What SIPC Protects" page, and the same page states plainly that SIPC does not cover market-value declines. That pairing is where the most common beginner misunderstanding lives. It is also why this guide was drafted with the SIPC page open first: subtract the $250,000 cash cap from the $500,000 ceiling and at most $250,000 of room remains for missing securities, and not one dollar of it answers a stock that simply falls in price. With the boundary fixed, we cross-checked it against the FINRA BrokerCheck and Vanguard index-fund pages. The verify-protect-diversify order is simply what those three sources actually say.

A beginner's first instinct is usually to go straight to tickers and "best stocks." That is the wrong place to begin, because the first decision a new investor actually controls is not which stock to own; it is which firm holds the account and whether that firm is registered and clean. The first job is not to find a single idea. It is to build a repeatable setup that keeps avoidable mistakes small.

For a new reader, the sequence should be:

- verify the broker,

- understand what account protection actually covers,

- and start with a broad, low-cost core before making concentrated stock-selection decisions.

That framework is less exciting than chasing a stock tip, but it is much more durable.

Source Evidence Snapshot

The hero map now combines the three source-grounded checks: FINRA broker verification, SIPC's custody-protection boundary, and Vanguard's index-fund baseline. The body evidence then breaks out the two concepts beginners most often confuse: account protection versus market risk, and an index baseline versus concentrated stock selection.

Source-derived SIPC boundary map: Based on SIPC's "What SIPC Protects" page, captured 2026-04-09. It separates the `$500,000` per-customer ceiling, the `$250,000` cash sub-limit, and the no-market-loss boundary. Figures and coverage wording are source-derived; layout is editorial rendering.

Source-derived SIPC boundary map: Based on SIPC's "What SIPC Protects" page, captured 2026-04-09. It separates the `$500,000` per-customer ceiling, the `$250,000` cash sub-limit, and the no-market-loss boundary. Figures and coverage wording are source-derived; layout is editorial rendering.

Source-derived index baseline map: Based on Vanguard's index-funds page, captured 2026-04-09. It shows the benchmark-tracking role of an index mutual fund or ETF, plus the low-cost, diversified, passive baseline described by the source. Definitions are source-derived; layout is editorial rendering.

Source-derived index baseline map: Based on Vanguard's index-funds page, captured 2026-04-09. It shows the benchmark-tracking role of an index mutual fund or ETF, plus the low-cost, diversified, passive baseline described by the source. Definitions are source-derived; layout is editorial rendering.

Step 1: Verify the Broker Before You Fund the Account

The BrokerCheck layer in the hero map is the right place to start because it forces the boring but necessary work first: verify who is taking custody of the account assets.

That matters more than many new readers expect. A smooth app experience does not tell you whether a firm is properly registered or whether there is disciplinary history worth reviewing. BrokerCheck exists precisely because "easy to use" and "safe to trust" are not the same question.

A clean beginner workflow is:

- identify the broker you plan to use,

- run the firm and, when relevant, the adviser through BrokerCheck,

- and only then compare account features like recurring investments, fractional shares, and research tools.

Step 2: Understand What Protection Does and Does Not Mean

Many people hear that an account is protected and assume that means they cannot lose money. The SIPC page shows why that is wrong.

SIPC protection is about custody failure, not investment success. It helps when customer cash or securities are missing at a failed SIPC-member brokerage. It does not protect you if the stock you bought falls 20%, 40%, or 70%.

That distinction is important because it changes how you think about risk:

- broker risk is about custody, registration, and account structure,

- investment risk is about what you actually buy.

Readers should keep those two risks separate instead of treating "protected account" as "safe exposure."

Step 3: Use Broad Index Funds as the Baseline Before Picking Individual Stocks

The Vanguard page is not a neutral regulator source, but it is still useful for one reason: it clearly states the baseline case for index funds. Low costs, built-in diversification, and passive benchmark tracking are not marketing fluff. They are the practical reasons index funds are often used as a simple starting benchmark.

That does not mean individual stocks are forbidden. It means they should come after the beginner already has:

- a verified brokerage setup,

- a basic understanding of account protection,

- and a diversified core exposure.

For many new readers, that order reduces the chance of making the classic mistake: turning the first market experience into concentrated stock picking before any process exists.

A Lower-Friction Research Framework

The simplest durable structure is:

- build the core with a broad index fund or ETF,

- automate contributions on a fixed schedule,

- and only then study individual stocks if you want direct company exposure.

This structure is not about maximizing excitement. It is about surviving the first year with fewer avoidable errors.

What New Readers Usually Get Wrong

They optimize for app design instead of broker quality

A polished mobile app can make the account feel trustworthy, but the right check is still registration status, disclosures, and custody protections.

They confuse protection with return certainty

SIPC coverage can protect missing assets in a brokerage failure. It cannot protect a bad stock choice.

They start with stock picking before they have a process

A broad index core gives a new reader a way to study market exposure while learning. Starting with five conviction names usually does the opposite: it magnifies mistakes before any verification discipline exists.

What Changes the Research Framework

The first edge for a new investor is not a brilliant stock pick. It is process quality.

Verify the broker through BrokerCheck. Understand what SIPC protection really means. Start with a broad, low-cost index-fund core. Then add complexity only after the basic setup is sound.

Related tools: compare account setup trade-offs with the brokerage account guide, then use the fee drag calculator and compound interest calculator to see how cost and contribution discipline change the long-term baseline.

That approach looks slower at the beginning, but it usually produces fewer costly mistakes and a much more stable investing habit.