Tech & Tools

What BrokerCheck and SIPC Reveal Before You Fund an Investing App

Before you fund an investing app: check registration on BrokerCheck, confirm custody, and learn what SIPC actually protects. A source-first 2026 workflow.

Thesis

(Sources: Investor.gov - Check Out Your Investment Professional, FINRA BrokerCheck, SEC Investment Adviser Public Disclosure)

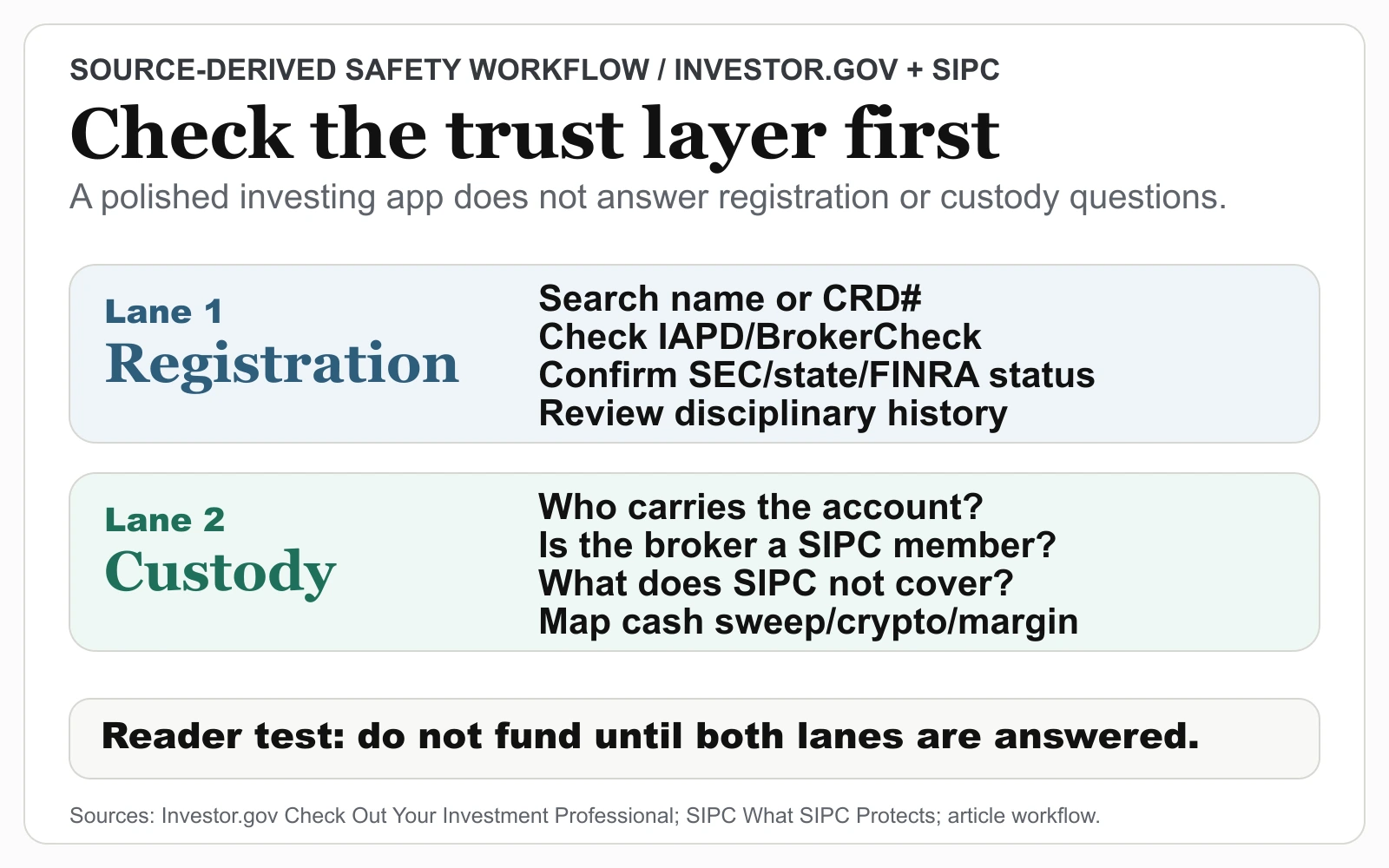

A single merged "safety workflow" was the first draft to get cut. The primary sources would not answer the same question: Investor.gov kept pointing toward registration and background checks, while the SIPC "What SIPC Protects" page held to a different one — its $500,000 limit, with the $250,000 cash sublimit, explicitly excludes market-value declines. Rather than force the merge, we worked each primary source in its own lane. The structure that survived traces where one stops answering and the other begins.

A brokerage app's onboarding screen is built to feel effortless, and that polish is exactly the problem: it answers none of the four questions that decide whether funding the account is safe. Before a dollar moves, the investor has to establish who is registered, who actually holds the assets, what protection applies, and — just as important — what protection explicitly does not.

That is why the practical workflow starts outside the app. Investor.gov, FINRA BrokerCheck, SEC Investment Adviser Public Disclosure, and SIPC are not growth features. They are the trust layer that lets a reader separate a legitimate investing workflow from a marketing interface.

This is especially important when a platform bundles brokerage, advisory tools, crypto, cash sweep, margin, options, or social trading features into one account experience. The product may look unified, but the legal protections can be segmented.

The 2026 editorial point is narrow: do not fund an investing app until the official registration lane and the custody-protection lane have both been checked. A product can be legitimate and still leave the user with misunderstood risks if those lanes are blended inside one interface.

Source Evidence Snapshot

The workflow map above anchors the registration and background-check lane. The SIPC map below anchors the separate custody-protection lane, so this article does not repeat the same visual evidence while making two different safety points.

Source-derived custody-boundary map: Based on SIPC's "What SIPC Protects" page, captured 2026-05-21. SIPC protection applies to eligible missing cash and securities at a failed SIPC-member brokerage firm, with a `$500,000` customer limit including a `$250,000` cash sublimit, and does not cover market-value declines or bad advice.

Source-derived custody-boundary map: Based on SIPC's "What SIPC Protects" page, captured 2026-05-21. SIPC protection applies to eligible missing cash and securities at a failed SIPC-member brokerage firm, with a `$500,000` customer limit including a `$250,000` cash sublimit, and does not cover market-value declines or bad advice.

These sources answer two different questions. Investor.gov addresses who the professional or firm is. SIPC addresses what happens to eligible customer assets if a SIPC-member brokerage firm fails and assets are missing. They are related, but they are not interchangeable.

What Changes the Workflow

The workflow changes only when the platform is not acting as a broker, adviser, or custodian at all. A pure portfolio tracker, tax tool, educational simulator, or market-data product may require different checks. For any product that takes orders, holds assets, manages portfolios, or introduces an investment professional, the official background and custody checks still matter.

Step 1: Verify the Person or Firm

Investor.gov directs users to check an investment professional's background and registration status and notes that users may be routed to IAPD or BrokerCheck depending on the professional or firm. That distinction matters.

Broker-dealers and their representatives are usually checked through FINRA BrokerCheck. Investment advisers are checked through IAPD, which is tied to SEC and state adviser registration. Some firms have both brokerage and advisory relationships, so the investor may need to look at both surfaces.

The practical questions are:

- Is the person or firm registered?

- In what capacity are they acting?

- Is the account brokerage, advisory, or both?

- Are there disclosures or disciplinary history that change the trust assessment?

This is not about finding a perfect record. It is about knowing the relationship before relying on the product.

Step 2: Separate Custody Protection From Investment Risk

SIPC is often misunderstood. SIPC is not a guarantee against losing money in stocks, funds, bonds, options, crypto, or other market exposures. The SIPC page states that protection is limited and that it does not protect against declines in the value of securities, bad investment advice, or inappropriate recommendations.

The protection frame is narrower: SIPC works to restore eligible missing cash and securities when a financially troubled SIPC-member brokerage firm is liquidated. SIPC states a $500,000 limit, including a $250,000 limit for cash. Read those two figures together: because the cash sublimit sits inside the total, the share of the $500,000 that can apply to missing securities is at most the $500,000 less the $250,000 cash portion — so cash held at the firm carries the tighter ceiling, and an account that parks a large balance in idle cash rather than securities can sit closer to the lower limit than the headline $500,000 suggests.

That means the safety question is not "can this account lose money?" All investment accounts can lose money. The better question is "if the brokerage firm fails and customer assets are missing, what customer protection layer applies?"

Step 3: Identify What Is Outside the Protection Frame

App-based investing often creates product bundling. A user may see stocks, ETFs, cash, options, crypto, lending, rewards, and automated portfolios in one interface. The protections can differ by product.

The key is to map the product to the legal relationship:

| App feature | Question to ask |

|---|---|

| Stock or ETF trading | Which broker-dealer carries the account, and is it a SIPC member? |

| Advisory portfolios | Which adviser manages the portfolio, and is it registered through SEC or state channels? |

| Cash sweep | Which bank or program holds the cash, and what insurance or sweep terms apply? |

| Crypto | Is the asset a security, commodity, wallet asset, or platform liability under the product terms? |

| Options or margin | What approval, risk disclosure, and liquidation rules apply? |

The interface may make these look like one account. The protection stack does not always work that way.

Common Pitfalls

The first pitfall is assuming that an app store presence equals financial registration. It does not. A polished interface is not a substitute for checking the firm or professional through official tools.

The second pitfall is treating SIPC like FDIC insurance. SIPC and FDIC solve different problems. SIPC is not designed to make investors whole after a market loss.

The third pitfall is ignoring product terms when crypto or cash sweep features are present. The legal holder, asset type, and protection scheme may differ from the headline account brand.

The fourth pitfall is relying on influencer or social-feed trust. A referral link can bring a user to a legitimate platform, but it does not answer registration, custody, or protection questions.

How to Apply This Before Funding an Account

A simple pre-funding checklist reduces the risk:

- Search the person or firm through Investor.gov routing, BrokerCheck, or IAPD.

- Confirm the registered entity name, not just the app brand.

- Read whether the account is brokerage, advisory, cash management, crypto, or a hybrid.

- Confirm whether the carrying brokerage is a SIPC member when securities custody is involved.

- Write down what SIPC does not cover, including market losses and bad advice.

- Read the margin, options, cash sweep, and crypto terms before enabling those features.

This process is not exciting, but it is fast. The point is to move the trust decision from brand design to documented legal relationships.

Final Check Before Funding

BrokerCheck, IAPD, Investor.gov, and SIPC are not optional footnotes for app-based investing. They are the pre-trade safety workflow.

The app tells the user what can be done. The official tools tell the user who is behind the relationship and what protection applies if something breaks. That distinction is the difference between using a modern investing tool and outsourcing trust to a screen.

Related tools: after the registration and custody checks, use the brokerage account guide to compare account features and the position size calculator to keep any first trade tied to a defined risk budget.