Green Transition

First Solar's 2026 Guidance Turns FSLR Into a Backlog-Conversion Test

First Solar's 2026 case lives or dies on backlog conversion, U.S. ASP assumptions, and cash discipline — measured against its own official guidance.

(Sources: Google Finance quote page for First Solar, First Solar Q4 2025 Earnings Presentation PDF)

Page 11 of First Solar's Q4 2025 earnings deck holds the 2026 guidance assumptions, not the summary slide everyone screenshots. That was the page we had open first — what management is committing to seemed worth knowing before grading the record year. One figure there set the terms for this note: the approximately 30.8 cents per watt U.S. ASP cited below. Cross-checking it against the 50.1 GW backlog and the $5.2 billion in 2025 net sales on the summary slide came afterward.

Related reading: The KRBN Wrapper Is the First Check Before Carbon Credit Exposure | What the 2026 FOMC Calendar Says About When Fed Cuts Can Come | Verify Your Broker Before You Pick a Single U.S. Stock

Thesis

Whether First Solar had a strong 2025 is no longer the interesting question. The official earnings deck makes that part obvious. The real test is whether the company can convert a very large backlog into another disciplined year while pricing, U.S. manufacturing execution, and policy assumptions all get harder.

The clearest evidence is on the company's own summary slide. First Solar said 2025 annual volume sold reached 17.5 GW, year-end backlog was 50.1 GW, record net sales were $5.2 billion, and diluted EPS reached $14.21. It also said gross cash ended the year at $2.9 billion and net cash at $2.4 billion.

That is why FSLR still commands more respect than the average solar name. This is not just a thematic policy trade. It is a manufacturer with scale, backlog visibility, and real cash.

At the same time, the 2026 guidance slide shows why the stock still has work to do. Management guided for 17.0 GW to 18.2 GW of volumes sold, approximately 30.8 cents per watt U.S. ASP, and working-capital reserves of $1.5 billion to $2.0 billion. That is a reminder that this year's story is no longer just about reporting a record year. It is about protecting economics through the next one.

Source Evidence Snapshot

The hero card already distills First Solar's 2025 summary highlights, so the body evidence stack keeps market context and 2026 guidance assumptions visual. The income-statement detail is retained as a source note to avoid repeating another earnings-deck screenshot with overlapping 2025 performance data.

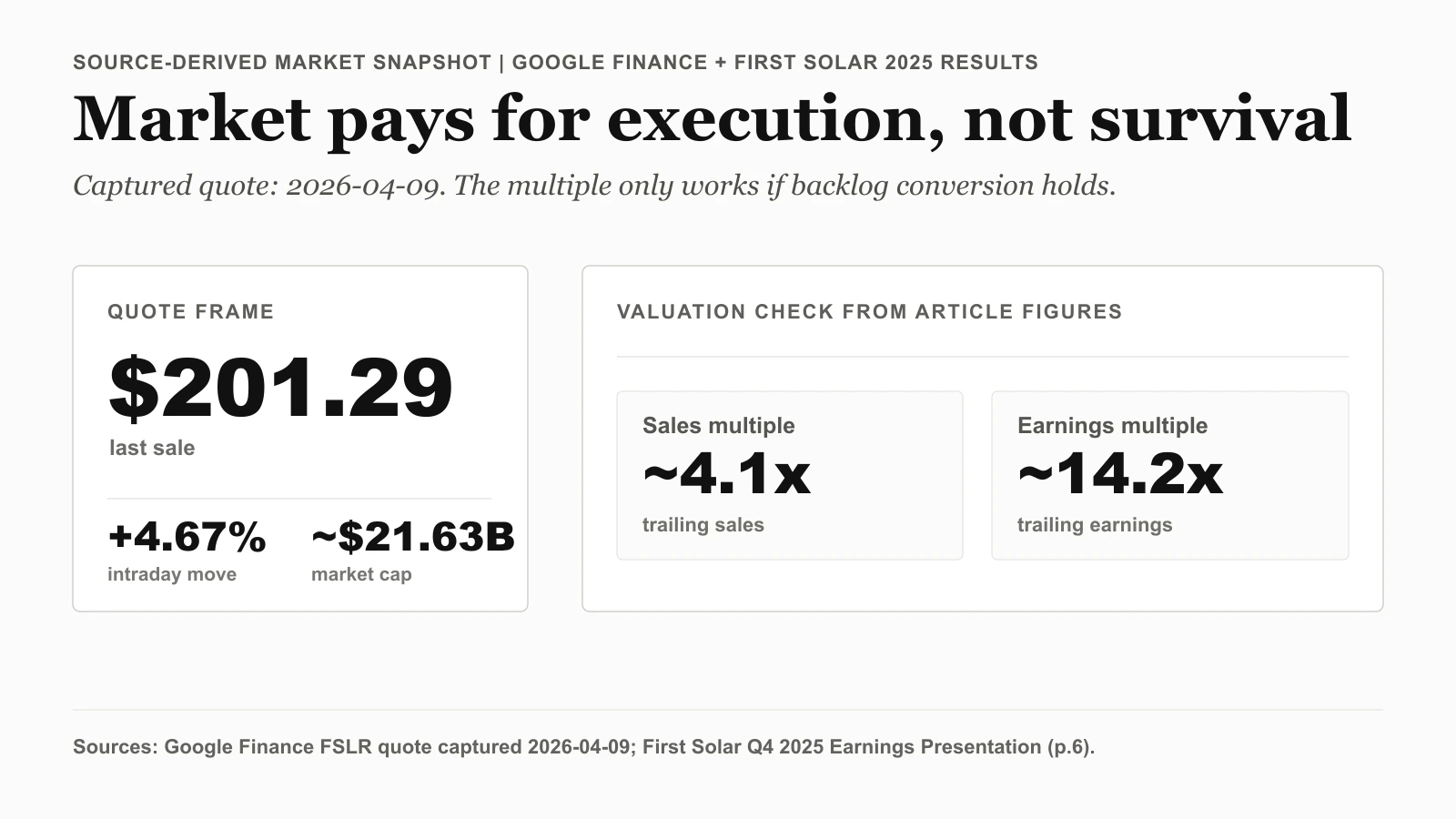

Source-derived market snapshot using the Google Finance quote page for First Solar, retrieved 2026-04-09, plus First Solar's 2025 net sales and net income from the Q4 2025 Earnings Presentation PDF, p.6. The numbers are the source's; the layout is ours.

The quote snapshot shows that the market is still willing to give First Solar a premium relative to weaker solar peers. In the captured view, FSLR traded at $201.29, up 4.67% on the day, with a market cap of about $21.63 billion. That is a valuation that assumes the backlog and U.S. manufacturing position are real advantages, not just temporary talking points.

Income-statement source note: First Solar Q4 2025 Earnings Presentation PDF, page 6, showed Q4 2025 net sales of $1.683 billion, gross profit percentage of 39.5%, net income of $521 million, and diluted EPS of 4.84. For the full year, the same slide showed net sales of $5.219 billion, net income of $1.528 billion, and diluted EPS of $14.21. That is why the stock is judged on execution quality rather than on mere survival.

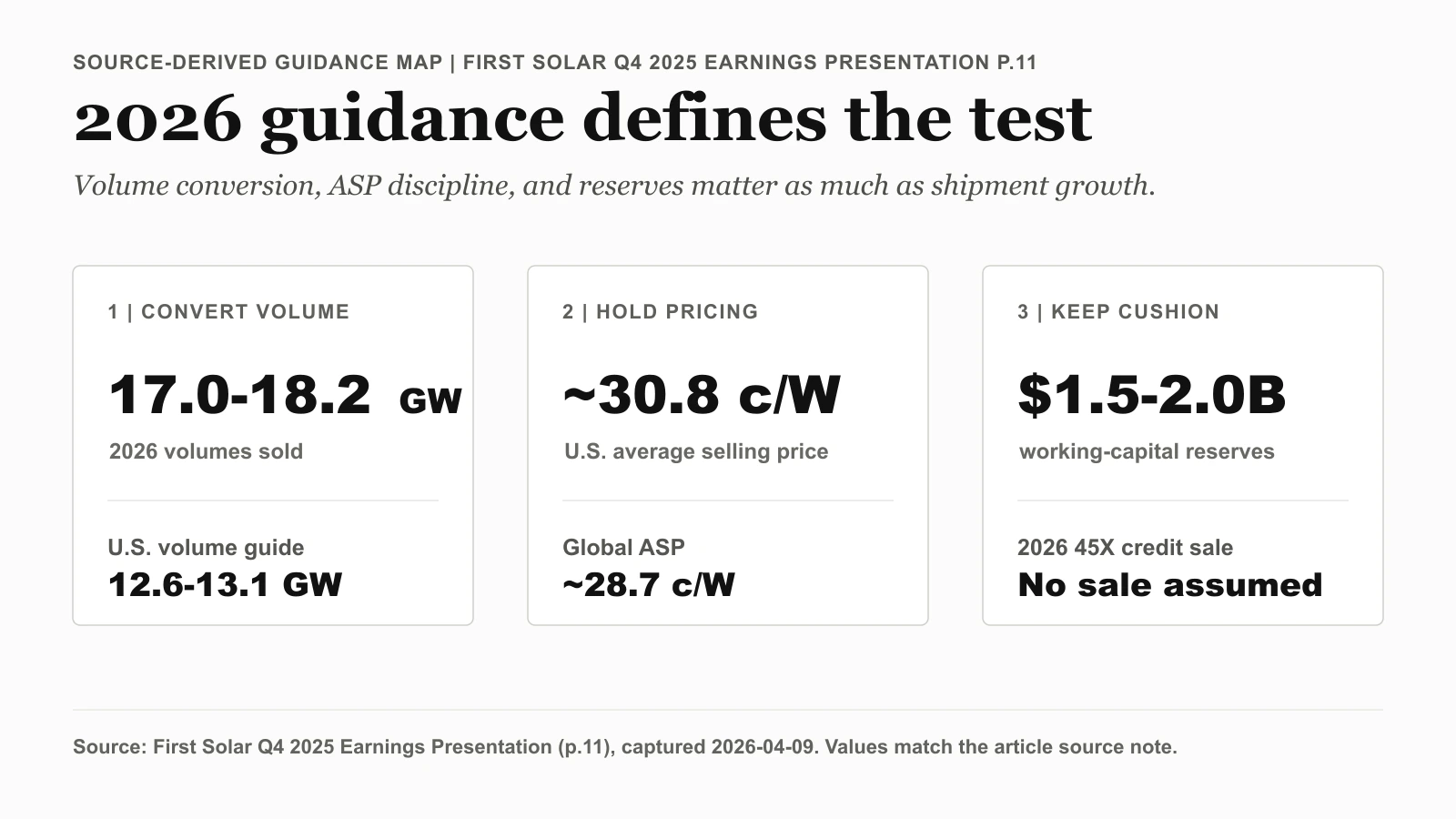

Evidence card based on First Solar's 2026 guidance — figures from the Q4 2025 Earnings Presentation PDF, p.11 (captured 2026-04-09). The numbers are the source's; the layout is ours.

The guidance slide is where the forward risk lives. First Solar guided for 17.0 GW to 18.2 GW of volumes sold, including 12.6 GW to 13.1 GW in the U.S., around 30.8 cents per watt U.S. ASP, about 28.7 cents per watt global ASP, no sale of 2026 Section 45X tax credits, and $1.5 billion to $2.0 billion of working-capital reserves. The evidence reads as a signal that pricing discipline and balance-sheet caution matter as much as shipment growth.

What the Street is Pricing

Put the price next to the financials and the premium stops being abstract. At the captured $21.63 billion market cap against $5.219 billion of 2025 net sales, the market is paying roughly 4.1 times trailing sales (21.63 ÷ 5.219). Against the $1.528 billion of full-year net income, that same cap is about 14.2 times trailing earnings (21.63 ÷ 1.528) — and the $201.29 share price divided by the $14.21 diluted EPS lands at the same place, near 14.2 times. So the Street is not assigning First Solar a distressed-solar multiple; it is paying a mid-teens earnings multiple for a profitable manufacturer with a contracted backlog.

That multiple is the whole debate. A ~14x trailing earnings tag is only defensible if 2026 holds the line, because management's own guidance bounds the volume — 17.0 GW to 18.2 GW of shipments at roughly 30.8 cents per watt U.S. ASP — rather than promising reacceleration. The premium does not survive ASP erosion or a working-capital squeeze; it survives backlog converting at the prices management already put on the slide.

Backlog Conversion Is Still the Core Debate

The 50.1 GW backlog number matters because it makes the revenue story less dependent on quarter-to-quarter sentiment. First Solar is not trying to win on hope alone. It already has a large book of business sitting in front of revenue recognition.

That backlog also fits the company's broader strategic advantage. First Solar is one of the few large-scale solar manufacturers with a meaningful U.S. manufacturing footprint and a differentiated module technology. That does not make it immune to policy or pricing pressure, but it does make the company structurally different from lower-quality solar equities whose stories rely more heavily on external financing or commodity-style module cycles.

The summary slide reinforces that point. Volumes, backlog, revenue, EPS, and cash all moved together in a way that makes the business look coordinated, not fragile.

2025 Was Strong Because Profitability Stayed Documented

Solar names often look optically cheap after a rally or a correction, but the better filter is whether the income statement is actually strong enough to support the cycle.

First Solar's deck clears that bar. Net sales of $5.219 billion, full-year net income of $1.528 billion, and diluted EPS of $14.21 show that the business produced real earnings power in 2025. The Q4 gross profit percentage of 39.5% is especially useful because it tells you the company did not need to sacrifice economics just to post a record year on volume.

This is why FSLR still trades as a quality name inside a messy sector. It has enough profitability and cash to make the next year an execution problem, not a solvency problem.

Risks to the Thesis

The reason the analysis still needs discipline is that 2026 no longer starts from a low bar. After a record 2025, the market expects First Solar to protect pricing and convert backlog efficiently.

Management's own assumptions show the challenge. Volumes sold are guided to 17.0 GW to 18.2 GW, which is still large but not a dramatic reacceleration. U.S. ASP is expected to be around 30.8 cents per watt, while global ASP is expected to be about 28.7 cents per watt. The company also said it is forecasting no sale of 2026 Section 45X tax credits and plans to maintain $1.5 billion to $2.0 billion of working-capital reserves.

That mix of assumptions does not read like a management team trying to manufacture excitement. It reads like one trying to protect margins, pricing, and capital structure through a more demanding policy and cost environment. For a long-duration thesis, that restraint is not automatically negative. It is part of the case.

What Flips the Call

Three variables matter most from here.

First, watch whether backlog converts into shipments without forcing pricing concessions. If the company keeps its ASP discipline, the backlog remains a real strategic asset instead of just a headline number.

Second, watch whether U.S. manufacturing execution stays clean as more capacity comes online. The Louisiana facility and the South Carolina finishing line matter because they tie the operating story directly to domestic production credibility.

Third, watch capital discipline. The company is telling investors up front that it wants to hold meaningful working-capital reserves and is not assuming 2026 tax-credit sales. That is a conservative setup, and conservative setups often matter most when sector conditions turn less forgiving.

The official deck supports the view that First Solar remains one of the strongest operating names in public solar. But it also makes clear that 2026 is no longer about proving the business exists. It is about proving the company can keep converting that scale and backlog into disciplined returns under tougher assumptions.