Market & Macro

AI Data Center Delays Are a 2026 Chip-Demand Timing Problem, Not a Collapse

Project delays and power limits aren't the same as collapsing chip demand. A 2026 look at AI data-center supply, hyperscaler backlog, and what the evidence supports.

(Sources: S&P Global on data-center development risk, Gartner on power shortages constraining AI data centers, Microsoft FY2025 Q2 earnings call, Alphabet Q4 2025 earnings release, Gartner 2026 semiconductor forecast)

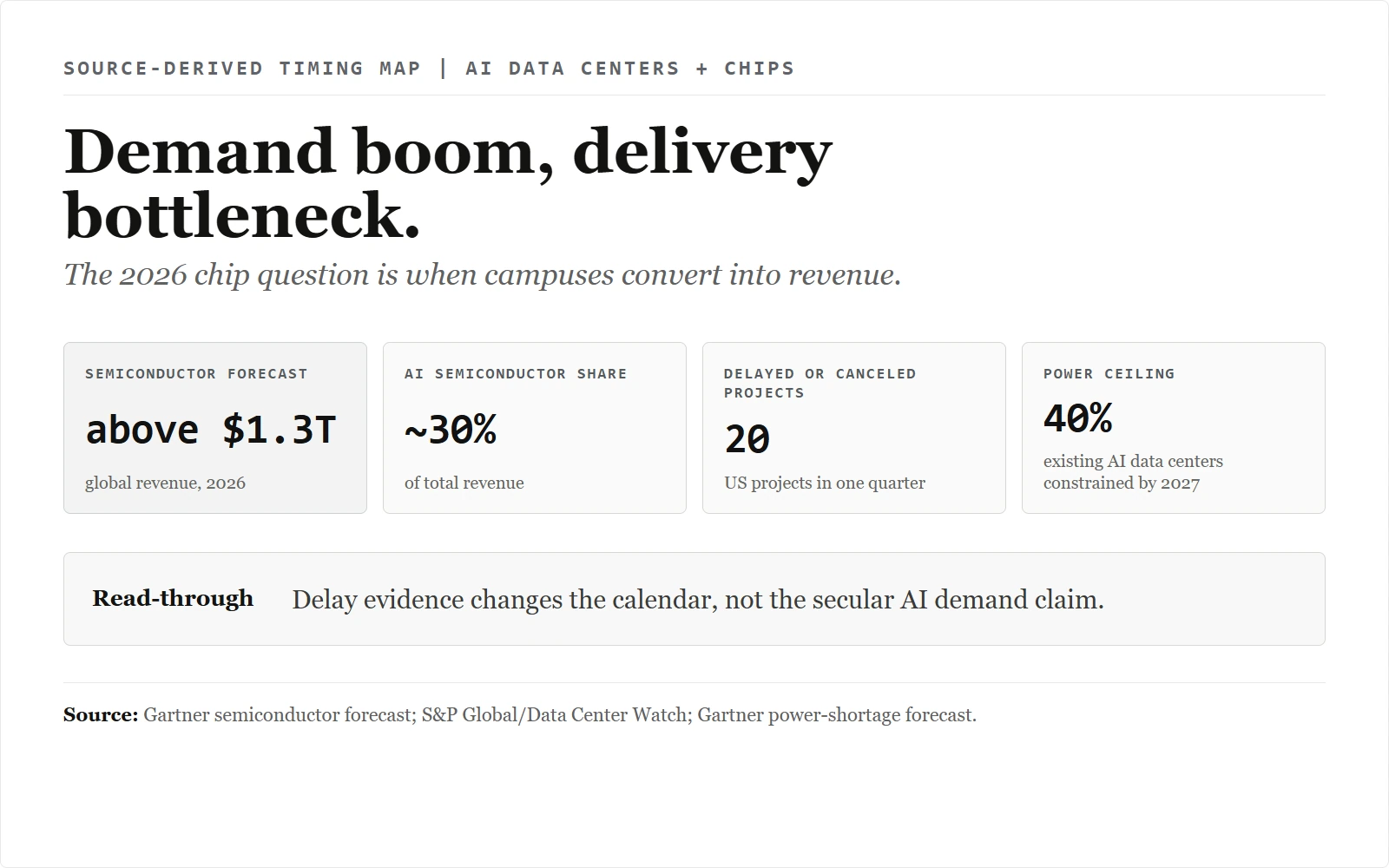

Twenty US data-center projects, delayed or canceled in a single quarter, sit in the same S&P Global article as 82.3 gigawatts of utility power demand it still expects from data centers in 2026. Two prints, one source, usually blurred together. Reconciling them was the first step in our process, and the gap read as supply timing slipping rather than demand falling — a read we then cross-checked against Gartner's warning that power could constrain 40% of existing AI data centers by 2027 before writing a word below.

Related reading: What the 2026 FOMC Calendar Says About When Fed Cuts Can Come | The KRBN Wrapper Is the First Check Before Carbon Credit Exposure | Verify Your Broker Before You Pick a Single U.S. Stock

AI data-center delays are now material enough to change semiconductor modeling. They do not prove that AI chip demand is fake. They do make one part of the 2026 setup more fragile: the assumption that every announced campus converts into same-year compute revenue.

The evidence points to a timing problem. S&P Global cited Data Center Watch data showing 20 US projects delayed or canceled in one quarter, while Gartner warned that power shortages could constrain 40% of existing AI data centers by 2027. At the same time, Microsoft still described cloud and AI spend tied to servers, CPUs, GPUs, and contracted backlog.

That combination makes the debate narrower and more useful. The risk is not necessarily a secular demand collapse. The risk is that part of the 2026 chip-demand curve has been pulled forward faster than power, grid access, and physical campuses can arrive.

Thesis

Treat the AI semiconductor debate as two separate questions rather than one. The first is whether AI workloads keep growing. The evidence from hyperscaler spending and Gartner's semiconductor forecast still supports that. The second is whether the physical buildout can turn that demand into chip revenue on the market's preferred calendar. That is where the risk is rising.

This article treats the delay evidence as a calendar-conversion risk, not as proof that the AI buildout has failed. That framing matters because it changes the analysis question from "Is AI demand real?" to "How much 2026 revenue assumes power and campuses arrive on schedule?"

Source Evidence Snapshot

The hero map now ties the broad Gartner semiconductor forecast to the physical delivery bottleneck. The body evidence keeps two non-overlapping layers: delayed projects and power constraints. Microsoft remains a linked source note because its capex and backlog material belongs mainly in the individual Microsoft stock article.

Source-derived project delay map: figures from S&P Global's article on data-center opposition and development risk, retrieved 2026-04-14. The highlighted figures show 20 delayed or canceled projects, about $100 billion in affected investment, utility power demand rising to 82.3 gigawatts in 2026, and the article's derived about $5 billion per project read-through. The numbers are the source's or direct arithmetic from the source figures; the layout is ours.

Open source.

Source-derived project delay map: figures from S&P Global's article on data-center opposition and development risk, retrieved 2026-04-14. The highlighted figures show 20 delayed or canceled projects, about $100 billion in affected investment, utility power demand rising to 82.3 gigawatts in 2026, and the article's derived about $5 billion per project read-through. The numbers are the source's or direct arithmetic from the source figures; the layout is ours.

Open source.

Source-derived power ceiling map: figure from the Gartner newsroom press release on AI data-center power shortages, retrieved 2026-04-14. The marked figure is Gartner's expectation that 40% of existing AI data centers could be constrained by power availability by 2027; the interpretation frames it as calendar slippage risk rather than demand-collapse proof. The number is the source's; the layout is ours.

Open source.

Source-derived power ceiling map: figure from the Gartner newsroom press release on AI data-center power shortages, retrieved 2026-04-14. The marked figure is Gartner's expectation that 40% of existing AI data centers could be constrained by power availability by 2027; the interpretation frames it as calendar slippage risk rather than demand-collapse proof. The number is the source's; the layout is ours.

Open source.

Source note: Microsoft FY2025 Q2 earnings call, captured 2026-04-14. Microsoft remains important context because it tied cloud and AI spend to servers, CPUs, GPUs, contracted backlog, and power/space constraints, but the macro page does not need a third body screenshot from a single company.

What the Street is Pricing

The market's optimistic AI semiconductor case assumes two things at once: demand keeps expanding, and the physical infrastructure arrives fast enough to convert that demand into near-term revenue. The first assumption still has support. The second is becoming more exposed.

S&P Global's cited delay data matters because project timing is not a smooth variable. A campus can remain financed and strategically important while still failing to convert into near-term chip demand if power, permitting, or grid equipment is late.

Size the stakes from the post's own figures: roughly $100 billion of affected investment spread across 20 delayed or canceled projects is about $5 billion of investment per project. That is not rounding error — it is heavy-capex, chip-intensive infrastructure, so each slipped project is the kind of line item a forecaster has to decide whether to keep in the 2026 column or push to 2027. The delay count is not a soft signal; it is a multi-billion-dollar timing question per project.

Gartner's power warning matters for the same reason. If a meaningful share of existing AI data centers can be constrained by power availability by 2027, then new capacity is not just a matter of ordering more chips. It depends on the slower layers of the physical stack.

Microsoft keeps the analysis from becoming too bearish. The company tied cloud and AI spend to servers, CPUs, GPUs, and contracted backlog while acknowledging shortages in power and space. Read together, that is a timing signal, not a demand signal: the spend is committed, but the same company naming power and space as the constraint tells you where the 2026 conversion risk actually sits.

Risks to the Thesis

The first risk is that the delay evidence gets overused. A delayed data center is not the same thing as canceled AI workload demand. Some chip purchases can shift later rather than disappear.

The second risk is that hyperscaler backlog proves stronger than the delay narrative. If short-lived server spend keeps rising and energized capacity ramps faster than expected, 2026 chip demand may remain more resilient than the bottleneck data implies.

The third risk is model granularity. Semiconductor estimates differ by supplier, product, backlog, customer exposure, and whether revenue is tied to live facilities or speculative future campuses. A broad delay headline can be analytically useful and still be too blunt for company-level conclusions.

What Flips the Call

The timing-risk case strengthens if more greenfield projects slip into 2027, utilities keep reporting longer power-connection queues, or hyperscalers keep spending heavily while more of the spend mix shifts toward buildings, power, and networking instead of immediately revenue-correlated servers.

The case weakens if Microsoft, Alphabet, and peers keep showing server backlog, short-lived compute assets, and actual energized capacity rising fast enough to absorb the buildout. It also weakens if semiconductor companies report demand that is increasingly tied to already powered facilities rather than announced but unresolved campuses.

The clean conclusion is narrower than the headline debate. Data-center delays do not prove that AI chips are a bubble. They do show that part of the 2026 demand curve may be too front-loaded. In a crowded AI infrastructure theme, that timing distinction is large enough to matter.