Market & Macro

NVDA's $102.7 Billion Cash Engine Now Has to Carry the AI Premium

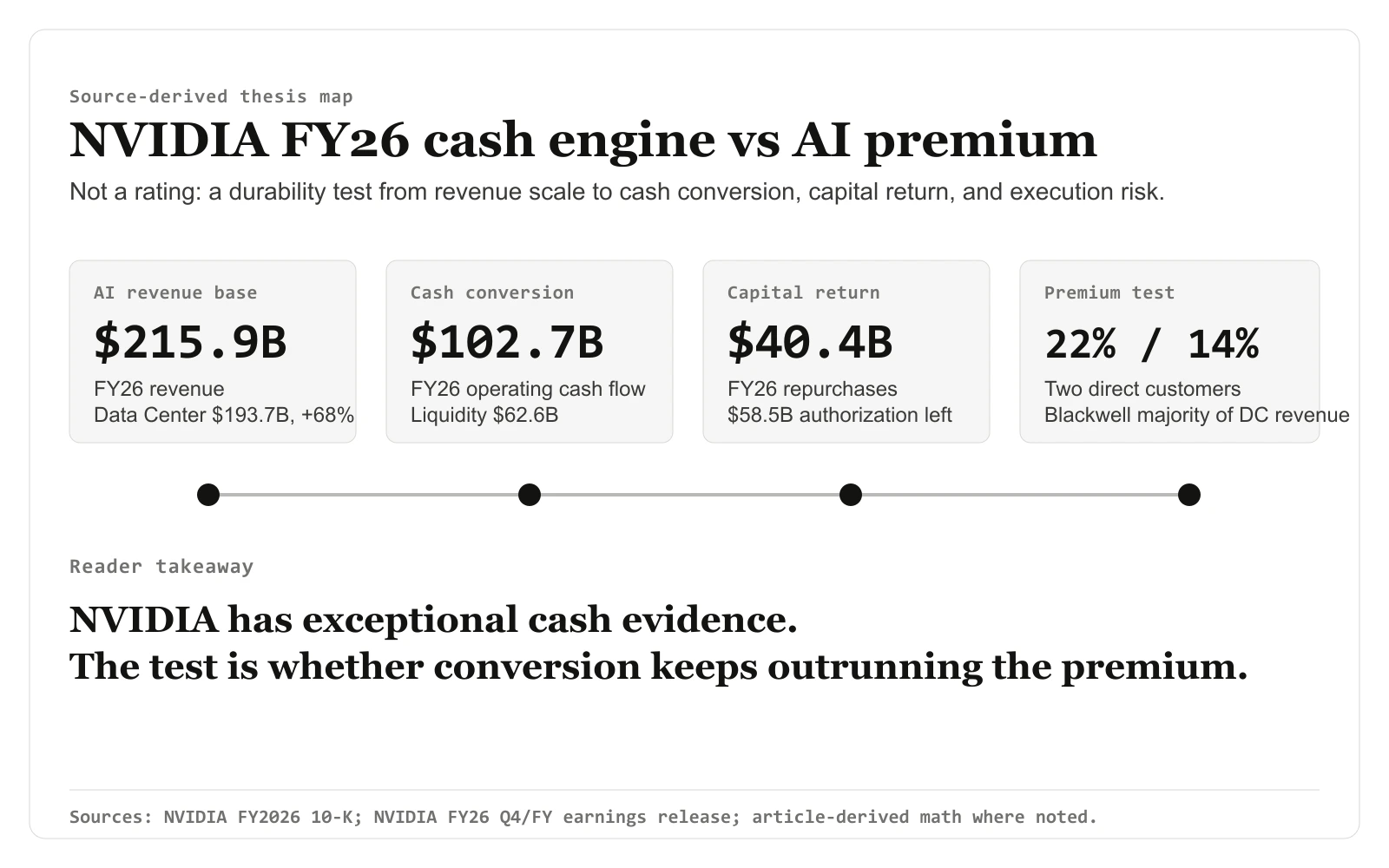

NVIDIA's FY2026 filings show $102.7 billion of operating cash flow, $62.6 billion of liquidity, and $40.4 billion of buybacks. The 2026 issue is whether that cash engine can defend an AI premium that already assumes durable leadership.

(Sources: NVIDIA FY2026 Form 10-K, NVIDIA Q4/FY2026 earnings release)

The headline said 73% revenue beat; page 43 of the FY2026 10-K said $102.7 billion of operating cash flow. Two different stories inside the same set of filings. So we worked through the cash-flow statement before anything else, then traced it forward to the $40.4 billion of buybacks on page 33, checking whether that capital return was funded by surplus rather than narrative. Taken in that order, the filing stops asking whether AI demand is real and starts asking how long this cash conversion can keep outrunning a premium that already assumes it.

Related reading: What the 2026 FOMC Calendar Says About When Fed Cuts Can Come | The KRBN Wrapper Is the First Check Before Carbon Credit Exposure | Verify Your Broker Before You Pick a Single U.S. Stock

Thesis

The right way to read NVIDIA now is through two lenses: business quality and entry-price risk. The business quality is still unusually strong. The stock price already assumes that AI infrastructure leadership stays durable.

The filing evidence supports the cash-engine thesis. It does not remove valuation risk. The stock depends on whether operating cash flow, buybacks, and product execution can keep supporting a premium while Blackwell, Rubin, hyperscaler spending, export rules, and customer concentration all remain active variables.

Source Evidence Snapshot

Source-derived cash conversion map: figures from the NVIDIA FY2026 Form 10-K cash-flow statement and liquidity table: net cash provided by operating activities of $102.718B in FY2026 and $64.089B in FY2025, purchases related to property and equipment and intangible assets of $6.042B, and cash, cash equivalents, and marketable securities of $62.556B. Implied free cash flow is article-derived math from operating cash flow less capex and intangibles. Figures are source-derived; layout is editorial rendering. FY2026 Form 10-K

Source-derived cash conversion map: figures from the NVIDIA FY2026 Form 10-K cash-flow statement and liquidity table: net cash provided by operating activities of $102.718B in FY2026 and $64.089B in FY2025, purchases related to property and equipment and intangible assets of $6.042B, and cash, cash equivalents, and marketable securities of $62.556B. Implied free cash flow is article-derived math from operating cash flow less capex and intangibles. Figures are source-derived; layout is editorial rendering. FY2026 Form 10-K

The latest official filings do not read like a company struggling to convert AI demand into cash. NVIDIA reported fourth-quarter revenue of $68.1 billion, up 73% year over year, and record fourth-quarter Data Center revenue of $62.3 billion, up 75%. Full-year revenue reached $215.9 billion, while full-year Data Center revenue rose 68% to $193.7 billion.

The more important line sits deeper in the annual report. NVIDIA's fiscal 2026 operating cash flow was $102.7 billion. That number changes the framing. The debate is no longer whether the AI revenue base is real. It is how long this level of cash conversion can keep outrunning expectations.

Source-derived capital return map: figures from the NVIDIA FY2026 Form 10-K capital-return section and cash-flow statement: $60.0B repurchase authorization, $40.4B of FY2026 repurchases for 282 million shares, $58.5B remaining authorization, and $974M of dividends paid. The $96.6B implied free cash flow, 42% buyback-to-FCF ratio, 0.6x remaining-authorization-to-FCF ratio, and about $143 implied average repurchase price are article-derived math from those source values. Figures are source-derived; layout is editorial rendering. FY2026 Form 10-K

Source-derived capital return map: figures from the NVIDIA FY2026 Form 10-K capital-return section and cash-flow statement: $60.0B repurchase authorization, $40.4B of FY2026 repurchases for 282 million shares, $58.5B remaining authorization, and $974M of dividends paid. The $96.6B implied free cash flow, 42% buyback-to-FCF ratio, 0.6x remaining-authorization-to-FCF ratio, and about $143 implied average repurchase price are article-derived math from those source values. Figures are source-derived; layout is editorial rendering. FY2026 Form 10-K

The capital-return line is now part of the core evidence. NVIDIA's board approved an additional $60.0 billion repurchase authorization in August 2025. The company repurchased 282 million shares for $40.4 billion during fiscal 2026 and still had $58.5 billion remaining under authorization at year-end.

What the Street is Pricing

The market is pricing NVIDIA as a core winner in the AI infrastructure stack, not as an overlooked semiconductor franchise. That is reasonable given the official numbers, but it raises the burden of proof.

The annual report says Blackwell architectures represented the majority of Data Center revenue in fiscal 2026. That is strong evidence that the product cycle converted into revenue. It also means the next leg of the thesis depends on continued product leadership, continued hyperscaler capex, and enough data-center, power, and supply-chain capacity to keep deployments moving.

The same filing says sales to one direct customer represented 22% of revenue in fiscal 2026 and another direct customer represented 14%. Concentration is manageable when spending is accelerating. It becomes more uncomfortable if a small number of customers slow AI deployment schedules or shift more workloads toward custom silicon.

The buyback evidence should be read in the same disciplined way. A $40.4 billion repurchase program is meaningful because it was funded alongside growth investment, not because buybacks automatically make a premium stock inexpensive. Sizing it against the post's own cash math sharpens the point: the $40.4 billion returned in FY2026 is roughly 42% of the $96.6 billion of free cash flow the filing implies ($102.7 billion operating cash flow less $6.1 billion capex), so NVIDIA returned under half its surplus and still funded the build-out. The $58.5 billion remaining authorization is about 0.6x that single year of free cash flow — sized to be cleared in well under two years at FY2026 conversion, before any new authorization. The $40.4 billion spent on 282 million shares also pins the average repurchase price at roughly $143 per share, a fact the filing fixes whether or not the stock now trades above it. In a high-expectation name, capital return is best treated as proof of cash surplus and management confidence. It is not a substitute for continued Data Center execution, broad customer demand, or product-cycle leadership. If those operating supports weaken, the same repurchase line would matter less.

Public consensus targets were not part of the cited evidence, so this article does not create a valuation target. The observable pricing issue is that NVIDIA already trades as a premium AI leader, and that premium now needs ongoing cash conversion to stay defensible.

Risks to the Thesis

The first risk is AI infrastructure demand digestion. A company this central to hyperscaler capex can still be hit if customers pause to absorb capacity after a rapid buildout.

The second risk is product-cycle compression. Blackwell has already carried a large part of the fiscal 2026 Data Center growth case. The market will expect Rubin and later platforms to keep the performance and supply lead wide enough to protect pricing.

The third risk is export policy. NVIDIA's filings continue to warn that policy changes can reshape the addressable market quickly, especially around China.

The fourth risk is customer concentration. The business can still grow with concentrated customers, but the stock becomes more sensitive to the spending rhythm of a small group of buyers.

The fifth risk is valuation compression. Exceptional businesses can still produce poor stock outcomes when expectations outrun the cash engine.

What Flips the Call

The thesis improves if NVIDIA keeps converting AI infrastructure leadership into operating cash flow near fiscal 2026 scale, maintains strong liquidity after growth investment, keeps capital returns visible, and shows that Blackwell-to-Rubin execution broadens rather than narrows the customer base.

The thesis weakens if hyperscaler spending enters a longer digestion phase, customer concentration becomes more pronounced, export restrictions bite harder, or free-cash-flow conversion falls while the stock still prices uninterrupted AI leadership.

NVIDIA trades at a premium because the business is converting AI demand into cash at unusual scale. The unresolved test is whether that cash engine can keep carrying a valuation that already assumes continued leadership.