Market & Macro

Why SQQQ Can Fall While the NASDAQ-100 Also Falls

SQQQ's daily-reset math is documented, not mysterious. The narrow timing conditions where a 3x-inverse NASDAQ hedge stays structurally coherent in 2026.

(Sources: ProShares UltraPro Short QQQ fund profile and prospectus, SEC investor bulletin on leveraged and inverse ETFs, Nasdaq-100 official index page)

Does "short the NASDAQ" mean a position that simply gains when the index loses? The ProShares prospectus answers no, and the answer hangs on one word: daily. To check that before writing anything else, we laid the prospectus's reset language alongside the SEC bulletin's warning about holding periods longer than one day, then traced both through the two-day 100 → 90 → 99 path cited below — SQQQ ends down 9% while QQQ is also lower. The contradiction the filing forced was simple. Once the reset is daily, "short" and "gains when the index falls" are not the same claim.

Thesis

Strip away the ETF wrapper and SQQQ is a daily rebalanced derivative, not a stock and not a conventional investment. It is designed to deliver three times the inverse of the NASDAQ-100's one-day return.

The word that matters is daily. Once that word is treated as the central feature rather than a footnote, SQQQ stops looking like a durable bear-market holding and starts looking like a time-bounded hedge framework. The structure can behave as intended when direction, time horizon, and volatility all line up. It can still fail when the directional call is right but the path is too choppy.

How the Instrument Actually Works

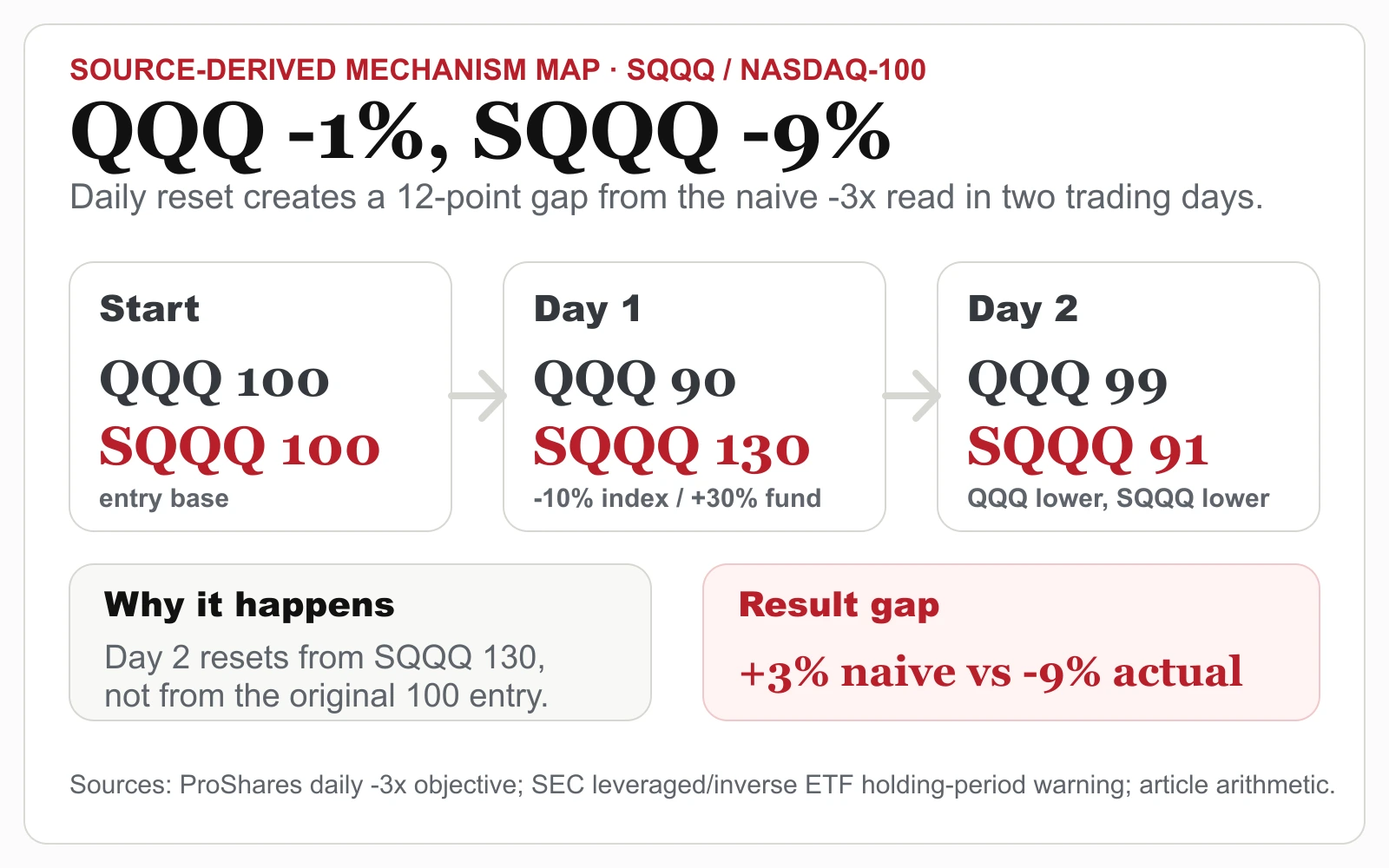

Every trading day, the fund manager resets the underlying exposure so that the next day targets roughly -3x the NASDAQ-100's daily return. If QQQ falls 1% today, SQQQ is designed to rise about 3% today. Tomorrow's exposure is then recomputed from the new closing NAV, not from the price the investor paid.

That makes the holding-period return path-dependent. A simple two-day example shows the problem. Suppose QQQ moves from 100 to 90, then back to 99. QQQ ends down 1%. A naive cumulative -3x read would imply SQQQ should be up about 3%. But the daily reset path is different: SQQQ moves from 100 to 130, then down 30% from that new base to 91. The position is down 9%, even though QQQ is also lower.

The daily mechanic itself is honest at each step: day one QQQ falls 10% (100 to 90) and SQQQ rises 30% (100 to 130), exactly -3x; day two QQQ rises 10% (90 to 99) and SQQQ falls 30% (130 to 91), again -3x. Both days hit the target. The damage lives entirely in the base that resets between them. The size of that damage is the number to internalize: the naive +3% expectation and the actual -9% outcome are 12 percentage points apart, and that 12-point wedge opened in just two trading days from a single round trip in the index. That is the cost of compounding from a new NAV rather than the entry price, made arithmetic rather than asserted.

That is volatility decay in its cleanest form. It is not a tracking error, a hidden fee, or a manager mistake. It is the product design doing exactly what it says it will do each day.

Source Evidence Snapshot

The proof stack here is documentary rather than a point-in-time quote snapshot:

- The ProShares SQQQ fund profile and prospectus are the issuer-level references. The repeated qualifier is daily exposure, which is the core reason the fund should not be read as a simple multi-week or multi-month short position.

- The SEC investor bulletin on leveraged and inverse ETFs is the plain-English risk baseline. It warns investors that leveraged and inverse ETFs can behave very differently from a simple multiple of index performance over periods longer than one day.

- The Nasdaq-100 official index page is the underlying-index reference. SQQQ inherits the index's concentration risk, so a move in a few mega-cap constituents can drive a large share of the daily return.

Source-derived use-case gate based on the ProShares SQQQ daily -3x objective and holding-period language, the SEC leveraged/inverse ETF investor bulletin, and the article's bounded-hedge framework.

Source-derived use-case gate based on the ProShares SQQQ daily -3x objective and holding-period language, the SEC leveraged/inverse ETF investor bulletin, and the article's bounded-hedge framework.

The clean framing is this: the structural facts are well documented and stable, while live trading-flow facts such as today's volume, AUM, borrow cost, and intraday spread are time-sensitive and should be checked in a broker or market-data screen before interpreting current market relevance.

What the Street is Pricing

Public sentiment data for SQQQ is not the same as sentiment data for a company. There are no operating earnings, no normal analyst-target surface in the stock sense, and no business model to value.

Three observable signals matter when current data is available:

- Daily volume versus average volume. A sharp spike usually marks hedging demand or speculation around a selloff, not a durable investment thesis.

- Short interest on SQQQ itself. Inverse ETFs can be shorted. Rising short interest while NASDAQ-100 volatility is low often means the market is leaning into continued grind-up conditions.

- NASDAQ-100 implied or realised volatility. Higher volatility makes the daily reset drag more damaging. Lower volatility can make a directional hedge cleaner when the index trends down steadily.

This is why SQQQ should be judged through tracking quality, expense ratio, liquidity, holding period, and volatility regime rather than a normal stock-style valuation framework.

When the Hedge Case Can Still Work

The thesis is narrow: SQQQ belongs in a time-bounded hedge framework, not a standing bearish allocation. That framework is most coherent in three specific regimes.

- A steady bear trend with low realised volatility. If the NASDAQ-100 falls persistently while daily volatility stays muted, the daily reset can work with the holder for a limited window. Confirming signal: the index keeps making lower lows while realised daily moves remain relatively orderly.

- A genuine intraday crash. A single large NASDAQ-100 down day can make SQQQ useful before decay compounds. Confirming signal: the index gaps down hard while volatility spikes on the same day.

- A tightly defined account hedge. In account-level risk control, a small SQQQ overlay can sometimes be compared with direct shorting when the underlying exposure cannot be hedged directly. Confirming signal: the hedge size and holding period are explicitly capped before use.

Outside those regimes, decay is usually the dominant force. The directional view can be correct and the hedge can still be poorly structured.

What Changes the SQQQ Case

The cleanest flip variable is the joint reading of NASDAQ-100 trend and volatility. If the NASDAQ-100 breaks lower in an orderly trend while realised volatility stays contained, the tactical hedge case briefly improves. If the market is choppy, gap-prone, or rangebound, the daily reset remains the central risk.

The product itself is not broken. The common mistake is using a one-day instrument as if it were a long-term bear-market investment. The prospectus and SEC bulletin matter because they force the analysis back to structure, path dependence, and the possibility that the investor can be right on direction but wrong on holding period.

Related tools: if a short-term hedge still fits the account rules, size it with the position size calculator and use the portfolio rebalancing calculator to keep the hedge from becoming a permanent allocation by accident.