Market & Macro

What AI Coding Agents Mean for Palo Alto Networks (PANW) Stock

Palo Alto Networks' Q2 ARR and RPO evidence against its valuation — and whether AI coding agents widen the attack surface PANW sells into. A 2026 read.

(Sources: Google Finance PANW quote page, Palo Alto Networks fiscal second quarter 2026 earnings release, OpenAI for developers, Anthropic Claude Code)

The fiscal Q2 2026 release carries the one line the AI-security story has to live or die on — Next-Generation Security ARR — and it read $6.3 billion. That figure got pinned down before anything else on the desk. The Google Finance quote panel came second; we used it to size the premium against that ARR line, which is where the $126.30 billion market cap and roughly 86.23 trailing P/E cited below come from. The coding-agent pages stayed as linked backdrop rather than evidence, since neither one shows up in PANW's revenue.

Related reading: What the 2026 FOMC Calendar Says About When Fed Cuts Can Come | The KRBN Wrapper Is the First Check Before Carbon Credit Exposure | Verify Your Broker Before You Pick a Single U.S. Stock

Thesis

Read PANW as an argument about who owns the security control plane, not as a generic cybersecurity-theme bet.

Coding agents such as Codex and Claude Code can pressure parts of the software stack. They can make code easier to write, test, and ship, which can compress value in tools whose main purpose is repetitive implementation work. That does not make an enterprise security platform less necessary. If AI increases code output, cloud activity, identity sprawl, and model usage, the enforcement layer can become more important.

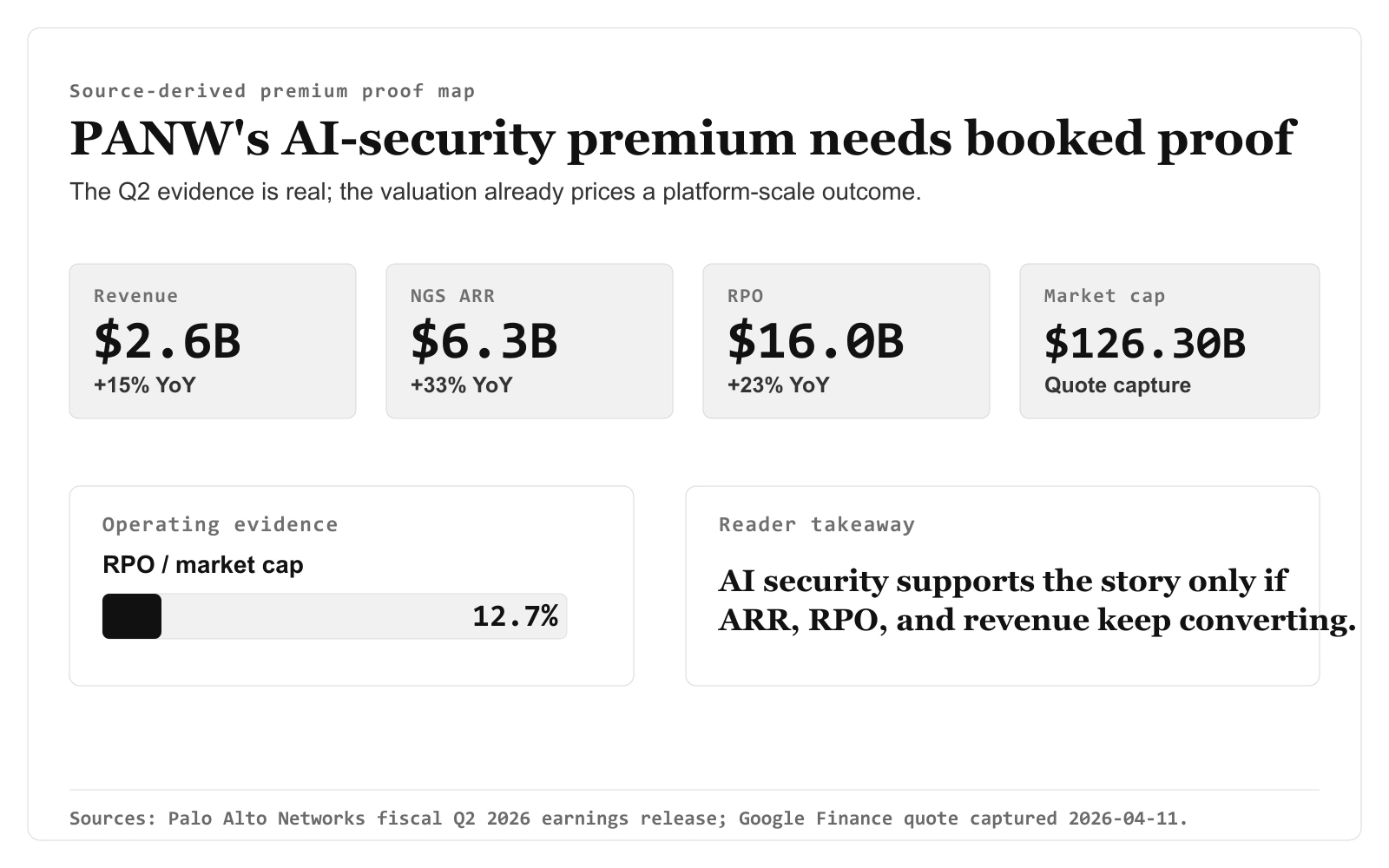

The fiscal Q2 2026 release gives the company-specific evidence. Palo Alto Networks reported $2.6 billion of revenue, $6.3 billion of Next-Generation Security ARR, and $16.0 billion of remaining performance obligation.

The valuation already assumes PANW can operate as a platform-scale security provider. The question is whether AI security turns that premium into a defendable business case rather than a crowded software multiple.

Source Evidence Snapshot

The hero map now carries the proof sequence the AI-security premium has to defend: Q2 revenue, Next-Generation Security ARR, RPO, market capitalization, and the RPO-to-market-cap gap. The body evidence keeps two visual layers: valuation burden and platform capacity. Coding-agent pages are treated as linked context because they explain industry backdrop rather than direct PANW revenue evidence.

Source-derived valuation burden map: figures from the Google Finance PANW quote page captured 2026-04-11 and Palo Alto Networks' fiscal Q2 2026 earnings release. The visual carries PANW around $155.73, market cap near $126.30B, trailing P/E around 86.23, annualized revenue of about $10.4B from Q2 revenue, market cap to Next-Generation Security ARR of about 20.0x, and market cap to annualized revenue of about 12.1x. Ratios are article-derived math; layout is editorial rendering.

Google Finance quote |

Fiscal Q2 2026 release.

Source-derived valuation burden map: figures from the Google Finance PANW quote page captured 2026-04-11 and Palo Alto Networks' fiscal Q2 2026 earnings release. The visual carries PANW around $155.73, market cap near $126.30B, trailing P/E around 86.23, annualized revenue of about $10.4B from Q2 revenue, market cap to Next-Generation Security ARR of about 20.0x, and market cap to annualized revenue of about 12.1x. Ratios are article-derived math; layout is editorial rendering.

Google Finance quote |

Fiscal Q2 2026 release.

This panel frames the burden of proof. A company valued near $126.30 billion needs more than a broad "cybersecurity is important" story. It needs evidence that its platform captures incremental complexity.

Source-derived platform capacity map: figures from Palo Alto Networks' fiscal Q2 2026 earnings release: cash and cash equivalents of $4.158B, long-term deferred revenue of $6.181B, GAAP net income of $432M, and fiscal-year 2026 adjusted free cash flow margin outlook of 37%. Figures are source-derived; layout is editorial rendering.

Fiscal Q2 2026 release.

Source-derived platform capacity map: figures from Palo Alto Networks' fiscal Q2 2026 earnings release: cash and cash equivalents of $4.158B, long-term deferred revenue of $6.181B, GAAP net income of $432M, and fiscal-year 2026 adjusted free cash flow margin outlook of 37%. Figures are source-derived; layout is editorial rendering.

Fiscal Q2 2026 release.

The balance sheet matters because security-platform consolidation is capital intensive. Cash, deferred revenue, and GAAP profitability give PANW more room to invest through product cycles than a narrower story stock would have.

Linked context, not a third proof image: OpenAI for developers and Anthropic Claude Code present coding agents as tools for building, editing, testing, and shipping code. That backdrop supports the attack-surface question, but it should not be read as evidence that coding agents directly create PANW revenue.

What the Street is Pricing

The captured quote page showed PANW around $155.73, a market cap near $126.30 billion, and a trailing P/E around 86.23. That is a premium setup.

The current evidence set does not include a verified short-interest panel, so this article does not frame PANW as a squeeze or positioning trade. The pricing question is simpler: the market is already paying a high multiple for durable security-platform demand, and the official Q2 2026 release has to keep justifying that premium with ARR, RPO, deferred revenue, and profitability.

Put the post's own numbers against each other and the premium gets concrete. The $126.30 billion market cap is roughly 20× the $6.3 billion Next-Generation Security ARR line the AI-security story has to live on (126.30 ÷ 6.3 ≈ 20.0). Said plainly: the market is valuing PANW at about twenty years of its current AI-security ARR, before any of the broader-attack-surface thesis shows up. The $16.0 billion of remaining performance obligation — the demand already contracted and on the books — covers only about an eighth of that market value (16.0 ÷ 126.30 ≈ 12.7%). The other roughly seven-eighths of the valuation is the market paying for growth that is not yet booked. That is the burden of proof in one ratio.

The market is paying for a company that can convert security complexity into platform growth. The official Q2 2026 release supports that claim with $6.3 billion of Next-Generation Security ARR, $16.0 billion of remaining performance obligation, and GAAP net income of $432 million. Run the same arithmetic on revenue: $2.6 billion of quarterly revenue annualizes to about $10.4 billion (2.6 × 4), which puts the $126.30 billion cap near 12× annualized sales (126.30 ÷ 10.4 ≈ 12.1). To judge whether that 12× sales and ~20× NGS-ARR pairing is rich or fair, the reader should pull the comparable price-to-sales and ARR multiples for CrowdStrike, Fortinet, and Zscaler — figures this post deliberately does not assert.

The Street is also pricing breadth. PANW is not only a firewall vendor in this framing. It spans network security, cloud security, security operations, identity, and AI security. That breadth is what makes the coding-agent discussion relevant. If AI makes enterprise software creation faster and more distributed, the security control plane may need to cover more surfaces, not fewer.

This is also why the article trims softer signals and keeps the evidence stack focused on valuation, contracted demand, balance-sheet capacity, and the AI-agent backdrop.

The premium therefore rests on a specific claim: AI is not only a software-labor disruptor. It is also a security-complexity multiplier.

Risks to the Thesis

The first risk is valuation. At a premium multiple, PANW can disappoint even if the business remains strong. Slower revenue growth, weaker ARR momentum, or lower security-budget urgency can compress the stock's multiple.

The second risk is that AI-security demand proves less incremental than management's language suggests. If AI security mainly repackages normal renewal activity, the market may demand a lower multiple.

The third risk is competition. CrowdStrike, Fortinet, Zscaler, and other security vendors are strong enough that PANW does not get a free win. Platform breadth helps, but it also requires execution across more surfaces.

The fourth risk is customer consolidation fatigue. Large enterprises may want fewer vendors, but they also resist platform lock-in if pricing, integration, or product overlap becomes too heavy.

What Flips the Call

The PANW setup improves if AI-security demand keeps appearing in hard metrics: Next-Generation Security ARR, RPO, deferred revenue, cloud and security-operations adoption, and GAAP profitability.

The setup weakens if coding agents become a broad software-multiple headwind without producing measurable incremental security demand for PANW, or if competitors capture the cleaner parts of AI security before Palo Alto Networks can turn breadth into share.

For now, coding agents are not best read as direct substitutes for Palo Alto Networks. They are better read as a force that can expand the systems enterprises need to secure. PANW's premium depends on proving that this wider control-plane role keeps translating into numbers.